- 西瓜云2

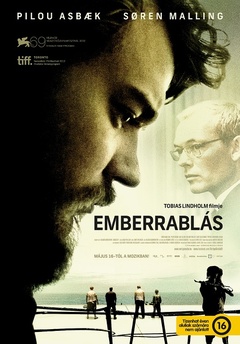

- 西瓜云1

- 正片

- 正片

怒海劫运

- 主演:

- 皮鲁·埃斯贝克/索伦·莫灵/达尔·萨利姆/罗兰·默勒

- 备注:

- 正片

- 类型:

- 喜剧片 剧情,惊悚

- 导演:

- 托比亚斯·林道赫姆

- 年代:

- 2012

- 地区:

- 丹麦

- 语言:

- 其他

- 更新:

- 2023-06-18 23:14

- 简介:

- 一群索马利亚海盗劫持了丹麦货船“罗森号”,船只航行在印度洋上,天气很好,海盗有恃无恐,时间宝贵是西方的概念,他们只在乎赎金。“罗森号”所属的总公司CEO是商场谈判高手,决定亲上火线和海盗周旋,他唯一被要求的重点就是保持冷静。问题是,世上没有一家航运学校曾教过学生如何对.....详细

一群索马利亚海盗劫持了丹麦货船“罗森号”,船只航行在印度洋上,天气很好,海盗有恃无恐,时间宝贵是西方的概念,他们只在乎赎金。“罗森号”所属的总公司CEO是商场谈判高手,决定亲上火线和海盗周旋,他唯一被要求的重点就是保持冷静。问题是,世上没有一家航运学校曾教过学生如何对付海盗,冷静在燠热的船舱是不被考虑的选项。电影通过两条线索展开,一条围绕着船上的厨师米克尔,另一条围绕着在丹麦的公司办公室里与海盗进行谈判的CEO彼得。

`•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.•´¯`•.¸¸.•´¯`•.•´¯`•.¸ ><((((º> 電影開始的時候,大廚說:你們知道為什麼我做的飯這麼好吃麼? -It's because I have a secret ingredient. Do you know what it is? - Love. `•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.•´¯`•.¸¸.•´¯`•.•´¯`•.¸ ><((((º> 看完電影,如果問:什麼是談判成功的秘方? -耐心 `•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.•´¯`•.¸¸.•´¯`•.•´¯`•.¸ ><((((º> 現實生活中多數人都不懂什麼是“利害”。比如,有很多會問:船員的生命是能夠拿冷冰冰的金錢、數字來衡量的嗎?這根本就是問錯了問題! 真正的問題,在於難平的欲壑之上,如何“利害相權”,搭起一座難搭的橋,堪堪能渡過難關。 的確,海盜手中有槍。但是,這並不改變談判雙方的對等位置! 這是一場心理的較量,真正唯一能改變雙方位置的,是雙方的心理。 談判中有兩種時間壓力,一是最後期限,一是時間成本。 海盜們沒有現代的“時間”觀念,因此海盜天然佔據一定的上風。 也因此伯克利畢業的談判專家特別提醒: Time is a western concept. It means nothing to them. 本片當中實際有兩場談判。一場是曠日持久的人質談判。還有一場是那場“意外”。 大談判總的來說很不容易,影片中展示了很多很經典的談判技巧: Do not show your emotions. If you do, they hold on you. If they come with threats, so ignore them. OK? Remember, we do not offer more money. It's their turn to go down now. We must continue to negotiate until we come to an agreement. 從數字來看,船公司的策略相當成功,而且讓步的步子幾乎是越邁越小,耐心得到了回報。如果不是當中CEO的情緒失控和海盜開槍,甚至有可能更加多快好省地達成目標: $250,000 (cap at <$5,000,000 --- I repeat. We must go down to less than five million before we can talk seriously.) $900,000 (+$650,000) $1,500,000 (+$600,000) $2,800,000 (+$1,300,000) (Note: after the the gun shot) $3,300,000 (+$500,000) ->Deal 反之海盜的步子越邁越大,也標識著他們在喪失耐心 $15,000,000 $12,000,000 (-$3,000,000) $8,500,000 (-$3,500,000) $3,300,000 (-$5,200,000) ->Deal 而丹麥人與海盜們的小談判卻談崩了,並因此帶來了意外的結果。原因可以從過程看得很明顯,就是因為不夠耐心。 但是你不能因此怪他們,因為船公司與海盜的整個談判過程都有專家團隊的專業指導,甚至即使這樣,在中間過程都還出了錯。 更重要的,所有丹麥人在”you have a deal”之後全都忘乎所以地高興起來,他們以為There’s a deal,認為海盜會嚴格細緻地按照協議來辦事。這就是今天典型的西方人的價值觀念。以船長為最典型,因為他不僅僅單純地相信了這個交易的可靠性,還恢復了他做為“船長——Captain”的自我意識。 所以中國人講話,即使談攏了,離開人家的會場之前,甚至在電梯里、廁所里也不要亂說話。 往深里說,是海盜們不懂“契約精神”嗎?錯!是丹麥人徹底忘記了“契約精神”是怎麼來的。 所謂的“契約精神”,絕不是“互相尊重”和“互惠互利”的結果,而是長時間“互相傷害”、“互相欺騙”的叢林法則下的產物。 要想形成“契約精神”,就得先讓不執行契約者明白其所付出的代價。 實際上,這最終是一種妥協精神。 而要讓人付出代價、學會妥協,就需要時間,就得學會耐心。 也因此在這個社會上倡導“契約精神”的,大多不是騙子,就是傻子。每遇到這種人,我總是敬鬼神而遠之。 別忘了,丹麥人的祖先們也是海盜。 `•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.•´¯`•.¸¸.•´¯`•.•´¯`•.¸ ><((((º> PS:之所以注意到這部影片,是因為看見了ft上很好的一篇文章,原文和譯文請參見: http://www.ft.com/intl/cms/s/0/1a322ad6-6293-11e3-bba5-00144feabdc0.html http://www.ft.com/intl/cms/s/0/1a322ad6-6293-11e3-bba5-00144feabdc0.html#axzz2tavuvqmD 談判“黃金守則”zz (注:請使用原鏈接,文章內容只是我不小心貼上去的) 作者:英國《金融時報》專欄作家 盧克•約翰遜 從我們小時候起,談判就在生活中發揮著極為重要的作用。為家庭作業而討價還價,為合租公寓、買車或商定勞動合同條款而討論條件——我們任何時候都離不開談判。 但談判科學是一門不受重視的學科,恐怕很少人真的以嚴謹態度或先見之明練習談判技巧。 毫無疑問,絕大多數人都會高估自己的談判能力。商業領袖應當尤其樂於提高自己的談判本領。 最近上映的一部電影,提醒我們在交易談判中應當遵守兩條黃金原則:一是要耐心,二是不能感情用事。 這部電影名叫《怒海劫運》(A Hijacking),講述了現代非洲海盜劫持了一艘丹麥貨船及其船員以勒索贖金的故事,非常驚心動魄。 我不會講述電影的情節,但它很值得一看,能教會我們在談判的過程中如何沉著應對,以達成更有利的結果——即便在利害攸關時也是如此。 已故的澳大利亞商人羅伯特•霍姆斯•阿•考特(Robert Holmes à Court)是一個很有手腕的人。他曾說:“有一個著名論斷是,你能判斷出誰將在談判中勝出,就是停頓時間最長的那一方。” 考特逐漸掌控了娛樂大亨盧•格拉德(Lew Grade)的娛樂帝國Associated Communications Corporation(簡稱ACC),但所付價錢僅為AAC內在價值的幾分之一,其中的操作手法經典地便體現了他的談判哲學。 牛市、杠桿以及寬松資金面使得一類談判者在許多交易中占據了主導地位:就是那些不斷報出比其他人更高價格的人。 在競購企業時,我們公司的報價總是比別人低。可能是我們太謹慎了。但從長遠看,總是出價最高很少真能奏效。 隨著經濟周期的輪動,企業的利潤水平和估值倍數有升有降。當然,如果你用的是別人的錢,那麽一擲千金就變得容易多了。 相比之下,我們公司掌管的大部分資金是自有資金,所以分配使用很嚴格。 最接近某項資產的人通常最瞭解它值多少錢:他們出價時,你就要當心了。我有幾次把公司賣給了內部人,之後經常感到後悔。 Twitter的創立,就是管理層以有利可圖的條件收購一家企業的經典案例。 埃文•威廉姆斯(Evan Williams)擁有一家名叫Odeo的初創企業,Twitter則是Odeo的附屬項目。 2006年,威廉姆斯告訴投資方,Odeo成不了氣候。他說:“我將繼續投資Twitter,可Twitter是否有資格得到像Odeo那樣的風險投資則很難說……” 因此,他提議由自己從投資方手中買下Odeo和Twitter的全部股權——據說只花了500萬美元。五年後,他購入的這些資產已價值50億美元。 如果我投資一家公司,總價只是考量因素之一。收購價看起來便宜,實際價值可能遠高於錶面價值,反之亦然。 管理層、資產負債表、商業潛力和與供應商的長期關系,都是影響收購意願和理由的要素。 通常說來,圍繞企業投資的談判會涉及方方面面,因為任何合同都涵蓋一系列復雜的要素:包括擔保條款、盡職調查,可能還有項目附帶權益。 大多數私人公司都很少出售,而且到下一次易主時公司可能已發生翻天覆地的變化。與此同時,專家估值多數情況下都只是基於充足信息的推測。 過去幾年裡,敲定一項交易所用時間比信貸危機之前長了一倍。在我看來,這是一個積極的變化:因為我在倉促投資時常會犯錯。 當你對一項交易感興趣,但並不會不惜代價去達成交易時,通常總能達成更有利的交易條款。你應當有一種控制力,使自己在交易條款令無法忍受時乾脆放棄。 無論對買家還是買家而言,擁有多種選擇無疑會比沒有備選項時將產生更有利的交易結果。對於任何交易而言,雙方在談判都感到滿意才可能會帶來完美結局。 譯者/邢嵬 `•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.•´¯`•.¸¸.•´¯`•.•´¯`•.¸ ><((((º> Patience is key to life’s endless negotiation By Luke Johnson `•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.•´¯`•.¸¸.•´¯`•.•´¯`•.¸ ><((((º> Executives who rush the process are likely to have a long time to dwell on their mistake `•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.•´¯`•.¸¸.•´¯`•.•´¯`•.¸ ><((((º> High quality global journalism requires investment. Please share this article with others using the link below, do not cut & paste the article. See our Ts&Cs and Copyright Policy for more detail. Email ftsales.support@ft.com to buy additional rights. http://www.ft.com/cms/s/0/1a322ad6-6293-11e3-bba5-00144feabdc0.html#ixzz2tc1osif0 Negotiation plays a central role in life from an early age. Haggles over homework, discussions about sharing an apartment, buying a car or agreeing terms for a job – we must all negotiate all the time. Yet the science of negotiation is an obscure discipline, and I fear few of us really practise it with much rigour or forethought. High quality global journalism requires investment. Please share this article with others using the link below, do not cut & paste the article. See our Ts&Cs and Copyright Policy for more detail. Email ftsales.support@ft.com to buy additional rights. http://www.ft.com/cms/s/0/1a322ad6-6293-11e3-bba5-00144feabdc0.html#ixzz2tc1uDtZ7 No doubt most of us believe that we are better negotiators than we really are. All business leaders should be especially willing to improve their techniques. A recent film serves as a powerful reminder about two of the golden rules in negotiating a deal: be patient and do not get emotionally involved. The film in question, A Hijacking , is a gripping tale about modern-day African pirates holding a Danish cargo ship and its crew to ransom. I won’t spoil the plot of the film, but it is well worth watching as a study in how to calmly draw out the bargaining to get a better deal – even when the stakes are very high indeed. The late Robert Holmes à Court, a master Australian wheeler dealer, once said: “It is a well-known proposition that you know who’s going to win a negotiation: it’s he who pauses longest.” The way in which he gradually managed to take control of impresario Lew Grade’s entertainment empire ACC for a fraction of its underlying value was a classic example of his philosophy in action. Bull markets, leverage and easy money have allowed a particular sort of negotiator to dominate in many situations: the guy who repeatedly offers more than anyone else. At my firm we are outbid all the time at auctions for companies. Perhaps we are too cautious. But consistently being the highest bidder rarely works in the long run. Economic cycles turn, and profits and multiples can fall as well as rise. Of course, it is a lot easier to pay lavish sums if you are using that wonderful material, other people’s money. By contrast, at our firm a lot of the cash on the table is ours, so it is strictly rationed. Those who are closest to an asset tend to know its worth best: be careful when they make you an offer. I have sold out of companies on a few occasions to insiders and often regretted it. The creation of Twitter is a fascinating example of management buying a business back on lucrative terms. Evan Williams had a start-up called Odeo – with a side project called Twitter. In 2006 Mr Williams told his investors that Odeo was going nowhere, saying “I will continue to invest in Twitter, but it’s hard to say it justifies the venture investment Odeo certainly holds...” So he made a proposal to buy them out – reputedly for $5m. Five years later, the assets he bought were priced at $5bn. If I invest in a company, the headline price is only one factor. An acquisition that appears cheap might actually be much more expensive than it seems, and vice versa. The management, balance sheet, commercial potential and continuing engagement of the vendor are among the many issues that influence one’s desire to buy, and the rationale of the purchase. Usually negotiations over a corporate investment are multifaceted, for any contract needs a complex set of elements: warranties, due diligence, perhaps a carried interest in the project. Most private companies sell only occasionally, and will probably have altered a lot by the time they next change hands. Meanwhile, expert valuations are mostly merely well-informed guesswork. Tying up a deal in the past few years has taken twice as long as it did before the credit crunch. For me that is a positive development: when I rush an investment I usually make mistakes. Inevitably you strike a better deal when you are keen but not desperate to close the transaction. If the terms are intolerable, then you should be able to walk away. Having a choice of options – whether as buyer or seller – will surely generate a better outcome than having no alternative to fall back on. And a negotiation that leaves both sides feeling good is perhaps the ideal conclusion of any exchange. `•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.•´¯`•.¸¸.•´¯`•.•´¯`•.¸ ><((((º>

"<>"" && "`•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.•´¯`•.¸¸.•´¯`•.•´¯`•.¸ ><((((º> 電影開始的時候,大廚說:你們知道為什麼我做的飯這麼好吃麼? -It's because I have a secret ingredient. Do you know what it is? - Love. `•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.•´¯`•.¸¸.•´¯`•.•´¯`•.¸ ><((((º> 看完電影,如果問:什麼是談判成功的秘方? -耐心 `•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.•´¯`•.¸¸.•´¯`•.•´¯`•.¸ ><((((º> 現實生活中多數人都不懂什麼是“利害”。比如,有很多會問:船員的生命是能夠拿冷冰冰的金錢、數字來衡量的嗎?這根本就是問錯了問題! 真正的問題,在於難平的欲壑之上,如何“利害相權”,搭起一座難搭的橋,堪堪能渡過難關。 的確,海盜手中有槍。但是,這並不改變談判雙方的對等位置! 這是一場心理的較量,真正唯一能改變雙方位置的,是雙方的心理。 談判中有兩種時間壓力,一是最後期限,一是時間成本。 海盜們沒有現代的“時間”觀念,因此海盜天然佔據一定的上風。 也因此伯克利畢業的談判專家特別提醒: Time is a western concept. It means nothing to them. 本片當中實際有兩場談判。一場是曠日持久的人質談判。還有一場是那場“意外”。 大談判總的來說很不容易,影片中展示了很多很經典的談判技巧: Do not show your emotions. If you do, they hold on you. If they come with threats, so ignore them. OK? Remember, we do not offer more money. It's their turn to go down now. We must continue to negotiate until we come to an agreement. 從數字來看,船公司的策略相當成功,而且讓步的步子幾乎是越邁越小,耐心得到了回報。如果不是當中CEO的情緒失控和海盜開槍,甚至有可能更加多快好省地達成目標: $250,000 (cap at <$5,000,000 --- I repeat. We must go down to less than five million before we can talk seriously.) $900,000 (+$650,000) $1,500,000 (+$600,000) $2,800,000 (+$1,300,000) (Note: after the the gun shot) $3,300,000 (+$500,000) ->Deal 反之海盜的步子越邁越大,也標識著他們在喪失耐心 $15,000,000 $12,000,000 (-$3,000,000) $8,500,000 (-$3,500,000) $3,300,000 (-$5,200,000) ->Deal 而丹麥人與海盜們的小談判卻談崩了,並因此帶來了意外的結果。原因可以從過程看得很明顯,就是因為不夠耐心。 但是你不能因此怪他們,因為船公司與海盜的整個談判過程都有專家團隊的專業指導,甚至即使這樣,在中間過程都還出了錯。 更重要的,所有丹麥人在”you have a deal”之後全都忘乎所以地高興起來,他們以為There’s a deal,認為海盜會嚴格細緻地按照協議來辦事。這就是今天典型的西方人的價值觀念。以船長為最典型,因為他不僅僅單純地相信了這個交易的可靠性,還恢復了他做為“船長——Captain”的自我意識。 所以中國人講話,即使談攏了,離開人家的會場之前,甚至在電梯里、廁所里也不要亂說話。 往深里說,是海盜們不懂“契約精神”嗎?錯!是丹麥人徹底忘記了“契約精神”是怎麼來的。 所謂的“契約精神”,絕不是“互相尊重”和“互惠互利”的結果,而是長時間“互相傷害”、“互相欺騙”的叢林法則下的產物。 要想形成“契約精神”,就得先讓不執行契約者明白其所付出的代價。 實際上,這最終是一種妥協精神。 而要讓人付出代價、學會妥協,就需要時間,就得學會耐心。 也因此在這個社會上倡導“契約精神”的,大多不是騙子,就是傻子。每遇到這種人,我總是敬鬼神而遠之。 別忘了,丹麥人的祖先們也是海盜。 `•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.•´¯`•.¸¸.•´¯`•.•´¯`•.¸ ><((((º> PS:之所以注意到這部影片,是因為看見了ft上很好的一篇文章,原文和譯文請參見: http://www.ft.com/intl/cms/s/0/1a322ad6-6293-11e3-bba5-00144feabdc0.html http://www.ft.com/intl/cms/s/0/1a322ad6-6293-11e3-bba5-00144feabdc0.html#axzz2tavuvqmD 談判“黃金守則”zz (注:請使用原鏈接,文章內容只是我不小心貼上去的) 作者:英國《金融時報》專欄作家 盧克•約翰遜 從我們小時候起,談判就在生活中發揮著極為重要的作用。為家庭作業而討價還價,為合租公寓、買車或商定勞動合同條款而討論條件——我們任何時候都離不開談判。 但談判科學是一門不受重視的學科,恐怕很少人真的以嚴謹態度或先見之明練習談判技巧。 毫無疑問,絕大多數人都會高估自己的談判能力。商業領袖應當尤其樂於提高自己的談判本領。 最近上映的一部電影,提醒我們在交易談判中應當遵守兩條黃金原則:一是要耐心,二是不能感情用事。 這部電影名叫《怒海劫運》(A Hijacking),講述了現代非洲海盜劫持了一艘丹麥貨船及其船員以勒索贖金的故事,非常驚心動魄。 我不會講述電影的情節,但它很值得一看,能教會我們在談判的過程中如何沉著應對,以達成更有利的結果——即便在利害攸關時也是如此。 已故的澳大利亞商人羅伯特•霍姆斯•阿•考特(Robert Holmes à Court)是一個很有手腕的人。他曾說:“有一個著名論斷是,你能判斷出誰將在談判中勝出,就是停頓時間最長的那一方。” 考特逐漸掌控了娛樂大亨盧•格拉德(Lew Grade)的娛樂帝國Associated Communications Corporation(簡稱ACC),但所付價錢僅為AAC內在價值的幾分之一,其中的操作手法經典地便體現了他的談判哲學。 牛市、杠桿以及寬松資金面使得一類談判者在許多交易中占據了主導地位:就是那些不斷報出比其他人更高價格的人。 在競購企業時,我們公司的報價總是比別人低。可能是我們太謹慎了。但從長遠看,總是出價最高很少真能奏效。 隨著經濟周期的輪動,企業的利潤水平和估值倍數有升有降。當然,如果你用的是別人的錢,那麽一擲千金就變得容易多了。 相比之下,我們公司掌管的大部分資金是自有資金,所以分配使用很嚴格。 最接近某項資產的人通常最瞭解它值多少錢:他們出價時,你就要當心了。我有幾次把公司賣給了內部人,之後經常感到後悔。 Twitter的創立,就是管理層以有利可圖的條件收購一家企業的經典案例。 埃文•威廉姆斯(Evan Williams)擁有一家名叫Odeo的初創企業,Twitter則是Odeo的附屬項目。 2006年,威廉姆斯告訴投資方,Odeo成不了氣候。他說:“我將繼續投資Twitter,可Twitter是否有資格得到像Odeo那樣的風險投資則很難說……” 因此,他提議由自己從投資方手中買下Odeo和Twitter的全部股權——據說只花了500萬美元。五年後,他購入的這些資產已價值50億美元。 如果我投資一家公司,總價只是考量因素之一。收購價看起來便宜,實際價值可能遠高於錶面價值,反之亦然。 管理層、資產負債表、商業潛力和與供應商的長期關系,都是影響收購意願和理由的要素。 通常說來,圍繞企業投資的談判會涉及方方面面,因為任何合同都涵蓋一系列復雜的要素:包括擔保條款、盡職調查,可能還有項目附帶權益。 大多數私人公司都很少出售,而且到下一次易主時公司可能已發生翻天覆地的變化。與此同時,專家估值多數情況下都只是基於充足信息的推測。 過去幾年裡,敲定一項交易所用時間比信貸危機之前長了一倍。在我看來,這是一個積極的變化:因為我在倉促投資時常會犯錯。 當你對一項交易感興趣,但並不會不惜代價去達成交易時,通常總能達成更有利的交易條款。你應當有一種控制力,使自己在交易條款令無法忍受時乾脆放棄。 無論對買家還是買家而言,擁有多種選擇無疑會比沒有備選項時將產生更有利的交易結果。對於任何交易而言,雙方在談判都感到滿意才可能會帶來完美結局。 譯者/邢嵬 `•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.•´¯`•.¸¸.•´¯`•.•´¯`•.¸ ><((((º> Patience is key to life’s endless negotiation By Luke Johnson `•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.•´¯`•.¸¸.•´¯`•.•´¯`•.¸ ><((((º> Executives who rush the process are likely to have a long time to dwell on their mistake `•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.•´¯`•.¸¸.•´¯`•.•´¯`•.¸ ><((((º> High quality global journalism requires investment. Please share this article with others using the link below, do not cut & paste the article. See our Ts&Cs and Copyright Policy for more detail. Email ftsales.support@ft.com to buy additional rights. http://www.ft.com/cms/s/0/1a322ad6-6293-11e3-bba5-00144feabdc0.html#ixzz2tc1osif0 Negotiation plays a central role in life from an early age. Haggles over homework, discussions about sharing an apartment, buying a car or agreeing terms for a job – we must all negotiate all the time. Yet the science of negotiation is an obscure discipline, and I fear few of us really practise it with much rigour or forethought. High quality global journalism requires investment. Please share this article with others using the link below, do not cut & paste the article. See our Ts&Cs and Copyright Policy for more detail. Email ftsales.support@ft.com to buy additional rights. http://www.ft.com/cms/s/0/1a322ad6-6293-11e3-bba5-00144feabdc0.html#ixzz2tc1uDtZ7 No doubt most of us believe that we are better negotiators than we really are. All business leaders should be especially willing to improve their techniques. A recent film serves as a powerful reminder about two of the golden rules in negotiating a deal: be patient and do not get emotionally involved. The film in question, A Hijacking , is a gripping tale about modern-day African pirates holding a Danish cargo ship and its crew to ransom. I won’t spoil the plot of the film, but it is well worth watching as a study in how to calmly draw out the bargaining to get a better deal – even when the stakes are very high indeed. The late Robert Holmes à Court, a master Australian wheeler dealer, once said: “It is a well-known proposition that you know who’s going to win a negotiation: it’s he who pauses longest.” The way in which he gradually managed to take control of impresario Lew Grade’s entertainment empire ACC for a fraction of its underlying value was a classic example of his philosophy in action. Bull markets, leverage and easy money have allowed a particular sort of negotiator to dominate in many situations: the guy who repeatedly offers more than anyone else. At my firm we are outbid all the time at auctions for companies. Perhaps we are too cautious. But consistently being the highest bidder rarely works in the long run. Economic cycles turn, and profits and multiples can fall as well as rise. Of course, it is a lot easier to pay lavish sums if you are using that wonderful material, other people’s money. By contrast, at our firm a lot of the cash on the table is ours, so it is strictly rationed. Those who are closest to an asset tend to know its worth best: be careful when they make you an offer. I have sold out of companies on a few occasions to insiders and often regretted it. The creation of Twitter is a fascinating example of management buying a business back on lucrative terms. Evan Williams had a start-up called Odeo – with a side project called Twitter. In 2006 Mr Williams told his investors that Odeo was going nowhere, saying “I will continue to invest in Twitter, but it’s hard to say it justifies the venture investment Odeo certainly holds...” So he made a proposal to buy them out – reputedly for $5m. Five years later, the assets he bought were priced at $5bn. If I invest in a company, the headline price is only one factor. An acquisition that appears cheap might actually be much more expensive than it seems, and vice versa. The management, balance sheet, commercial potential and continuing engagement of the vendor are among the many issues that influence one’s desire to buy, and the rationale of the purchase. Usually negotiations over a corporate investment are multifaceted, for any contract needs a complex set of elements: warranties, due diligence, perhaps a carried interest in the project. Most private companies sell only occasionally, and will probably have altered a lot by the time they next change hands. Meanwhile, expert valuations are mostly merely well-informed guesswork. Tying up a deal in the past few years has taken twice as long as it did before the credit crunch. For me that is a positive development: when I rush an investment I usually make mistakes. Inevitably you strike a better deal when you are keen but not desperate to close the transaction. If the terms are intolerable, then you should be able to walk away. Having a choice of options – whether as buyer or seller – will surely generate a better outcome than having no alternative to fall back on. And a negotiation that leaves both sides feeling good is perhaps the ideal conclusion of any exchange. `•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.•´¯`•.¸¸.•´¯`•.•´¯`•.¸ ><((((º>

"<>"暂时没有网友评论该影片"}`•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.•´¯`•.¸¸.•´¯`•.•´¯`•.¸ ><((((º> 電影開始的時候,大廚說:你們知道為什麼我做的飯這麼好吃麼? -It's because I have a secret ingredient. Do you know what it is? - Love. `•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.•´¯`•.¸¸.•´¯`•.•´¯`•.¸ ><((((º> 看完電影,如果問:什麼是談判成功的秘方? -耐心 `•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.•´¯`•.¸¸.•´¯`•.•´¯`•.¸ ><((((º> 現實生活中多數人都不懂什麼是“利害”。比如,有很多會問:船員的生命是能夠拿冷冰冰的金錢、數字來衡量的嗎?這根本就是問錯了問題! 真正的問題,在於難平的欲壑之上,如何“利害相權”,搭起一座難搭的橋,堪堪能渡過難關。 的確,海盜手中有槍。但是,這並不改變談判雙方的對等位置! 這是一場心理的較量,真正唯一能改變雙方位置的,是雙方的心理。 談判中有兩種時間壓力,一是最後期限,一是時間成本。 海盜們沒有現代的“時間”觀念,因此海盜天然佔據一定的上風。 也因此伯克利畢業的談判專家特別提醒: Time is a western concept. It means nothing to them. 本片當中實際有兩場談判。一場是曠日持久的人質談判。還有一場是那場“意外”。 大談判總的來說很不容易,影片中展示了很多很經典的談判技巧: Do not show your emotions. If you do, they hold on you. If they come with threats, so ignore them. OK? Remember, we do not offer more money. It's their turn to go down now. We must continue to negotiate until we come to an agreement. 從數字來看,船公司的策略相當成功,而且讓步的步子幾乎是越邁越小,耐心得到了回報。如果不是當中CEO的情緒失控和海盜開槍,甚至有可能更加多快好省地達成目標: $250,000 (cap at <$5,000,000 --- I repeat. We must go down to less than five million before we can talk seriously.) $900,000 (+$650,000) $1,500,000 (+$600,000) $2,800,000 (+$1,300,000) (Note: after the the gun shot) $3,300,000 (+$500,000) ->Deal 反之海盜的步子越邁越大,也標識著他們在喪失耐心 $15,000,000 $12,000,000 (-$3,000,000) $8,500,000 (-$3,500,000) $3,300,000 (-$5,200,000) ->Deal 而丹麥人與海盜們的小談判卻談崩了,並因此帶來了意外的結果。原因可以從過程看得很明顯,就是因為不夠耐心。 但是你不能因此怪他們,因為船公司與海盜的整個談判過程都有專家團隊的專業指導,甚至即使這樣,在中間過程都還出了錯。 更重要的,所有丹麥人在”you have a deal”之後全都忘乎所以地高興起來,他們以為There’s a deal,認為海盜會嚴格細緻地按照協議來辦事。這就是今天典型的西方人的價值觀念。以船長為最典型,因為他不僅僅單純地相信了這個交易的可靠性,還恢復了他做為“船長——Captain”的自我意識。 所以中國人講話,即使談攏了,離開人家的會場之前,甚至在電梯里、廁所里也不要亂說話。 往深里說,是海盜們不懂“契約精神”嗎?錯!是丹麥人徹底忘記了“契約精神”是怎麼來的。 所謂的“契約精神”,絕不是“互相尊重”和“互惠互利”的結果,而是長時間“互相傷害”、“互相欺騙”的叢林法則下的產物。 要想形成“契約精神”,就得先讓不執行契約者明白其所付出的代價。 實際上,這最終是一種妥協精神。 而要讓人付出代價、學會妥協,就需要時間,就得學會耐心。 也因此在這個社會上倡導“契約精神”的,大多不是騙子,就是傻子。每遇到這種人,我總是敬鬼神而遠之。 別忘了,丹麥人的祖先們也是海盜。 `•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.•´¯`•.¸¸.•´¯`•.•´¯`•.¸ ><((((º> PS:之所以注意到這部影片,是因為看見了ft上很好的一篇文章,原文和譯文請參見: http://www.ft.com/intl/cms/s/0/1a322ad6-6293-11e3-bba5-00144feabdc0.html http://www.ft.com/intl/cms/s/0/1a322ad6-6293-11e3-bba5-00144feabdc0.html#axzz2tavuvqmD 談判“黃金守則”zz (注:請使用原鏈接,文章內容只是我不小心貼上去的) 作者:英國《金融時報》專欄作家 盧克•約翰遜 從我們小時候起,談判就在生活中發揮著極為重要的作用。為家庭作業而討價還價,為合租公寓、買車或商定勞動合同條款而討論條件——我們任何時候都離不開談判。 但談判科學是一門不受重視的學科,恐怕很少人真的以嚴謹態度或先見之明練習談判技巧。 毫無疑問,絕大多數人都會高估自己的談判能力。商業領袖應當尤其樂於提高自己的談判本領。 最近上映的一部電影,提醒我們在交易談判中應當遵守兩條黃金原則:一是要耐心,二是不能感情用事。 這部電影名叫《怒海劫運》(A Hijacking),講述了現代非洲海盜劫持了一艘丹麥貨船及其船員以勒索贖金的故事,非常驚心動魄。 我不會講述電影的情節,但它很值得一看,能教會我們在談判的過程中如何沉著應對,以達成更有利的結果——即便在利害攸關時也是如此。 已故的澳大利亞商人羅伯特•霍姆斯•阿•考特(Robert Holmes à Court)是一個很有手腕的人。他曾說:“有一個著名論斷是,你能判斷出誰將在談判中勝出,就是停頓時間最長的那一方。” 考特逐漸掌控了娛樂大亨盧•格拉德(Lew Grade)的娛樂帝國Associated Communications Corporation(簡稱ACC),但所付價錢僅為AAC內在價值的幾分之一,其中的操作手法經典地便體現了他的談判哲學。 牛市、杠桿以及寬松資金面使得一類談判者在許多交易中占據了主導地位:就是那些不斷報出比其他人更高價格的人。 在競購企業時,我們公司的報價總是比別人低。可能是我們太謹慎了。但從長遠看,總是出價最高很少真能奏效。 隨著經濟周期的輪動,企業的利潤水平和估值倍數有升有降。當然,如果你用的是別人的錢,那麽一擲千金就變得容易多了。 相比之下,我們公司掌管的大部分資金是自有資金,所以分配使用很嚴格。 最接近某項資產的人通常最瞭解它值多少錢:他們出價時,你就要當心了。我有幾次把公司賣給了內部人,之後經常感到後悔。 Twitter的創立,就是管理層以有利可圖的條件收購一家企業的經典案例。 埃文•威廉姆斯(Evan Williams)擁有一家名叫Odeo的初創企業,Twitter則是Odeo的附屬項目。 2006年,威廉姆斯告訴投資方,Odeo成不了氣候。他說:“我將繼續投資Twitter,可Twitter是否有資格得到像Odeo那樣的風險投資則很難說……” 因此,他提議由自己從投資方手中買下Odeo和Twitter的全部股權——據說只花了500萬美元。五年後,他購入的這些資產已價值50億美元。 如果我投資一家公司,總價只是考量因素之一。收購價看起來便宜,實際價值可能遠高於錶面價值,反之亦然。 管理層、資產負債表、商業潛力和與供應商的長期關系,都是影響收購意願和理由的要素。 通常說來,圍繞企業投資的談判會涉及方方面面,因為任何合同都涵蓋一系列復雜的要素:包括擔保條款、盡職調查,可能還有項目附帶權益。 大多數私人公司都很少出售,而且到下一次易主時公司可能已發生翻天覆地的變化。與此同時,專家估值多數情況下都只是基於充足信息的推測。 過去幾年裡,敲定一項交易所用時間比信貸危機之前長了一倍。在我看來,這是一個積極的變化:因為我在倉促投資時常會犯錯。 當你對一項交易感興趣,但並不會不惜代價去達成交易時,通常總能達成更有利的交易條款。你應當有一種控制力,使自己在交易條款令無法忍受時乾脆放棄。 無論對買家還是買家而言,擁有多種選擇無疑會比沒有備選項時將產生更有利的交易結果。對於任何交易而言,雙方在談判都感到滿意才可能會帶來完美結局。 譯者/邢嵬 `•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.•´¯`•.¸¸.•´¯`•.•´¯`•.¸ ><((((º> Patience is key to life’s endless negotiation By Luke Johnson `•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.•´¯`•.¸¸.•´¯`•.•´¯`•.¸ ><((((º> Executives who rush the process are likely to have a long time to dwell on their mistake `•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.•´¯`•.¸¸.•´¯`•.•´¯`•.¸ ><((((º> High quality global journalism requires investment. Please share this article with others using the link below, do not cut & paste the article. See our Ts&Cs and Copyright Policy for more detail. Email ftsales.support@ft.com to buy additional rights. http://www.ft.com/cms/s/0/1a322ad6-6293-11e3-bba5-00144feabdc0.html#ixzz2tc1osif0 Negotiation plays a central role in life from an early age. Haggles over homework, discussions about sharing an apartment, buying a car or agreeing terms for a job – we must all negotiate all the time. Yet the science of negotiation is an obscure discipline, and I fear few of us really practise it with much rigour or forethought. High quality global journalism requires investment. Please share this article with others using the link below, do not cut & paste the article. See our Ts&Cs and Copyright Policy for more detail. Email ftsales.support@ft.com to buy additional rights. http://www.ft.com/cms/s/0/1a322ad6-6293-11e3-bba5-00144feabdc0.html#ixzz2tc1uDtZ7 No doubt most of us believe that we are better negotiators than we really are. All business leaders should be especially willing to improve their techniques. A recent film serves as a powerful reminder about two of the golden rules in negotiating a deal: be patient and do not get emotionally involved. The film in question, A Hijacking , is a gripping tale about modern-day African pirates holding a Danish cargo ship and its crew to ransom. I won’t spoil the plot of the film, but it is well worth watching as a study in how to calmly draw out the bargaining to get a better deal – even when the stakes are very high indeed. The late Robert Holmes à Court, a master Australian wheeler dealer, once said: “It is a well-known proposition that you know who’s going to win a negotiation: it’s he who pauses longest.” The way in which he gradually managed to take control of impresario Lew Grade’s entertainment empire ACC for a fraction of its underlying value was a classic example of his philosophy in action. Bull markets, leverage and easy money have allowed a particular sort of negotiator to dominate in many situations: the guy who repeatedly offers more than anyone else. At my firm we are outbid all the time at auctions for companies. Perhaps we are too cautious. But consistently being the highest bidder rarely works in the long run. Economic cycles turn, and profits and multiples can fall as well as rise. Of course, it is a lot easier to pay lavish sums if you are using that wonderful material, other people’s money. By contrast, at our firm a lot of the cash on the table is ours, so it is strictly rationed. Those who are closest to an asset tend to know its worth best: be careful when they make you an offer. I have sold out of companies on a few occasions to insiders and often regretted it. The creation of Twitter is a fascinating example of management buying a business back on lucrative terms. Evan Williams had a start-up called Odeo – with a side project called Twitter. In 2006 Mr Williams told his investors that Odeo was going nowhere, saying “I will continue to invest in Twitter, but it’s hard to say it justifies the venture investment Odeo certainly holds...” So he made a proposal to buy them out – reputedly for $5m. Five years later, the assets he bought were priced at $5bn. If I invest in a company, the headline price is only one factor. An acquisition that appears cheap might actually be much more expensive than it seems, and vice versa. The management, balance sheet, commercial potential and continuing engagement of the vendor are among the many issues that influence one’s desire to buy, and the rationale of the purchase. Usually negotiations over a corporate investment are multifaceted, for any contract needs a complex set of elements: warranties, due diligence, perhaps a carried interest in the project. Most private companies sell only occasionally, and will probably have altered a lot by the time they next change hands. Meanwhile, expert valuations are mostly merely well-informed guesswork. Tying up a deal in the past few years has taken twice as long as it did before the credit crunch. For me that is a positive development: when I rush an investment I usually make mistakes. Inevitably you strike a better deal when you are keen but not desperate to close the transaction. If the terms are intolerable, then you should be able to walk away. Having a choice of options – whether as buyer or seller – will surely generate a better outcome than having no alternative to fall back on. And a negotiation that leaves both sides feeling good is perhaps the ideal conclusion of any exchange. `•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.¸¸.•´¯`•.•´¯`•.¸¸.•´¯`•.•´¯`•.¸ ><((((º>